You finally found it. The house with the big backyard and the kitchen island you’ve always wanted. You have 8% saved up, which felt like a massive achievement until you sat down with your loan officer. Suddenly, they drop a bomb: you have to pay for mortgage loan insurance. It sounds like a safety net for your family, right? Like if you lose your job, the insurance pays the bill?

Wrong.

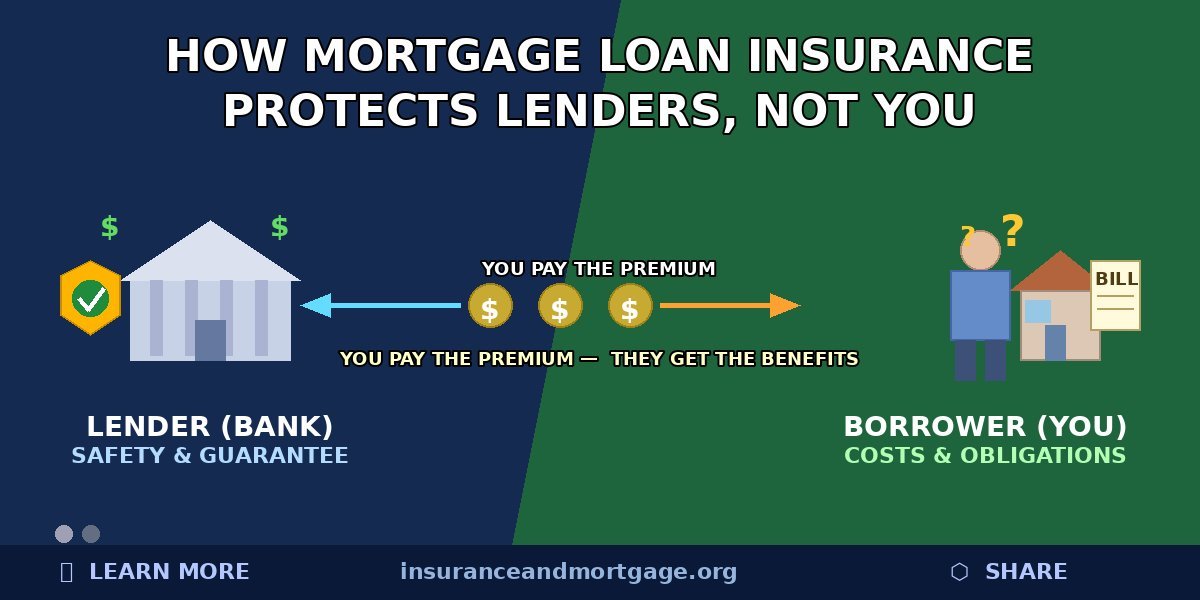

That is the biggest myth in real estate. This insurance is a one-way street. You pay the bill, but the bank gets all the peace of mind. In this guide, we’re going to pull back the curtain on how this system actually works. We’ll look at the hidden costs, the regional tax traps, and why “insured” borrowers sometimes get better interest rates than people with huge down payments. Let’s get into math.

What is Mortgage Loan Insurance?

Basically, it is a policy that covers the lender’s butt if you stop paying your mortgage. When you put down less than 20% of the home’s price, you are considered a “high-ratio” borrower. To a bank, you look risky. They worry that if the housing market dips, you won’t have enough skin in the game to keep paying.

In the United States, this is usually called Private Mortgage Insurance (PMI). In Canada, it’s often just called CMHC insurance, named after the biggest provider. Whether you are in Toronto or Texas, the deal is the same. You pay a premium so the bank feels safe giving you a pile of money.

The Providers: Who are the Players?

In Canada, three companies dominate the scene. The heavy hitter is the Canada Mortgage and Housing Corporation (CMHC), which is a crown corporation. Then you have Sagen and Canada Guaranty, which are private.

Down in the US, it’s all private players like Radian, MGIC, and Essent. Or, if you get a government-backed FHA loan, you pay a Mortgage Insurance Premium (MIP).

The $1 Million Hard Stop

Here is a quirky rule many people miss. In Canada, you cannot get mortgage loan insurance on a home that costs $1 million or more. If you want that luxury condo or a detached home in Vancouver, you must have 20% down. No exceptions. This rule keeps the government from backing the riskiest, most expensive loans.

Who Does This Policy Actually Benefit?

Let’s be blunt. You are the one writing the check, but you aren’t the beneficiary. If you default and the bank sells your house at a loss, the insurer pays the bank the difference.

But wait. There’s a catch.

The insurer doesn’t just say “thanks for the premium” and walk away. They can legally sue you to get back the money they paid to the bank. This is called subrogation. So, the house is gone, your credit is ruined, and the insurance company is still knocking on your door.

Why Lenders Love It

If it’s so bad for you, why does it exist? Because without it, most people couldn’t buy a home. Lenders wouldn’t touch a 5% down payment without this protection. It opens the door to homeownership, but the “entry fee” is steep.

The Real Cost: Breaking Down the Numbers

The cost depends on how much you put down. The less you provide upfront, the higher your premium. In Canada, these rates are standard across the board.

Canadian Premium Table (2024)

| Down Payment | Loan-to-Value (LTV) | Premium (% of Total Loan) |

| 5% | 95% | 4.00% |

| 10% | 90% | 3.10% |

| 15% | 85% | 2.80% |

| 20% or more | 80% or less | $0 (Not Required) |

Source: CMHC 2024 Rate Guide

In the US, PMI is usually a monthly fee rather than a lump sum. It typically costs between 0.5% and 1.5% of the loan amount annually. According to the Urban Institute, a borrower with a $300,000 loan might pay $125 to $375 every single month just for insurance.

The Interest Trap and the “PST” Surprise

Most people don’t pay the premium upfront. They add it to the mortgage. If your premium is $15,000, your $400,000 mortgage becomes $415,000.

But think about that for a second. You are now paying interest on that $15,000 for the next 25 years. At a 5% interest rate, that “small” premium actually costs you thousands more in interest over the life of the loan. It’s a double whammy.

The Sales Tax Sting

If you live in Ontario, Quebec, or Saskatchewan, you have another problem. These provinces charge Provincial Sales Tax (PST) on the insurance premium. Unlike the premium itself, you cannot add this tax to your mortgage. You have to pay it in cash to your lawyer on closing day. For a $500,000 home, that could be an extra $1,600 you didn’t plan for.

The Weird Perk: Lower Interest Rates

Here is a bit of a plot twist. Sometimes, having mortgage loan insurance actually gets you a better interest rate.

Wait, what?

Think like a bank. If a loan is insured, the bank has zero risk. If you fail, they get paid anyway. Because the loan is “backstopped,” they often offer a lower interest rate to insured borrowers compared to someone putting 20% down.

While the insurance premium is expensive, the lower interest rate can save you money on your monthly payments. You have to run the math to see which path wins.

Can You Ever Get Rid of It?

This is where the US and Canada go in different directions.

In the United States, the Homeowners Protection Act of 1998 is your best friend. Once your home equity hits 20% through mortgage payments or rising home values, you can ask the bank to cancel the PMI. At 22% equity, they usually have to cancel it automatically.

In Canada? You’re stuck. Once you pay that premium, it’s gone. You don’t get a refund when you hit 20% equity. However, the insurance is “portable.” If you buy a new house, you can often move the insurance to the new property without paying the full fee again.

What Happens During a Default?

Let’s look at the worst-case scenario. According to the CMHC 2023 Annual Report, the mortgage arrears rate in Canada is very low—around 0.28%. Most people pay their bills. But if you don’t, here is the chain of events:

- You miss payments and the lender starts the foreclosure process.

- The house is sold. Let’s say you owe $450,000 but the house only sells for $400,000.

- The insurer (like CMHC) pays the lender the $50,000 gap.

- The lender is happy. They have all their money.

- The insurer now owns your $50,000 debt. They will use debt collectors or court orders to get it from you.

Strategies to Avoid the Cost

Saving 20% is the obvious answer, but in today’s market, that’s hard. A $600,000 home requires $120,000 for a 20% down payment. That’s a lot of coffee you’d have to stop buying.

What else can you do?

- The “B-Lender” Route: Some alternative lenders will let you skip insurance with a smaller down payment, but they will charge you a much higher interest rate.

- Gifted Equity: Most lenders allow a gift from a family member to count toward your 20%. You just need a signed letter stating the money isn’t a loan.

- Lower Your Sights: Buying a cheaper starter home might let you hit that 20% mark sooner. You can then use the equity from that home to buy your “forever home” later without needing insurance.

Wrapping It Up

At the end of the day, mortgage loan insurance is a tool. It isn’t there to protect your house or your family’s finances. It is a security blanket for the bank. You are paying for their safety so they will take a chance on you.

Is it unfair? Maybe. But for many, it’s the only way to get a foot in the door of a wild housing market. Just make sure you factor in the interest costs and the potential PST at closing. Going in with your eyes open is the only way to ensure you don’t get blindsided by the true cost of your new home.