Here’s something most business executives don’t think about until it stings—insurance premiums. They come due all at once. And they’re not small. For many companies, a single annual insurance bill can run into tens of thousands of dollars. Sometimes much more. Paying it all upfront puts real pressure on your finances, especially when that money could work harder somewhere else in your business. That’s where premium funding changes the game. It is a practical solution that more businesses are adopting—and for good reason. In this guide, we will walk through why this matters. From cash flow management to tax tricks, there is more to this arrangement than most people realize. Let’s get into the details.

What Exactly Is Premium Funding?

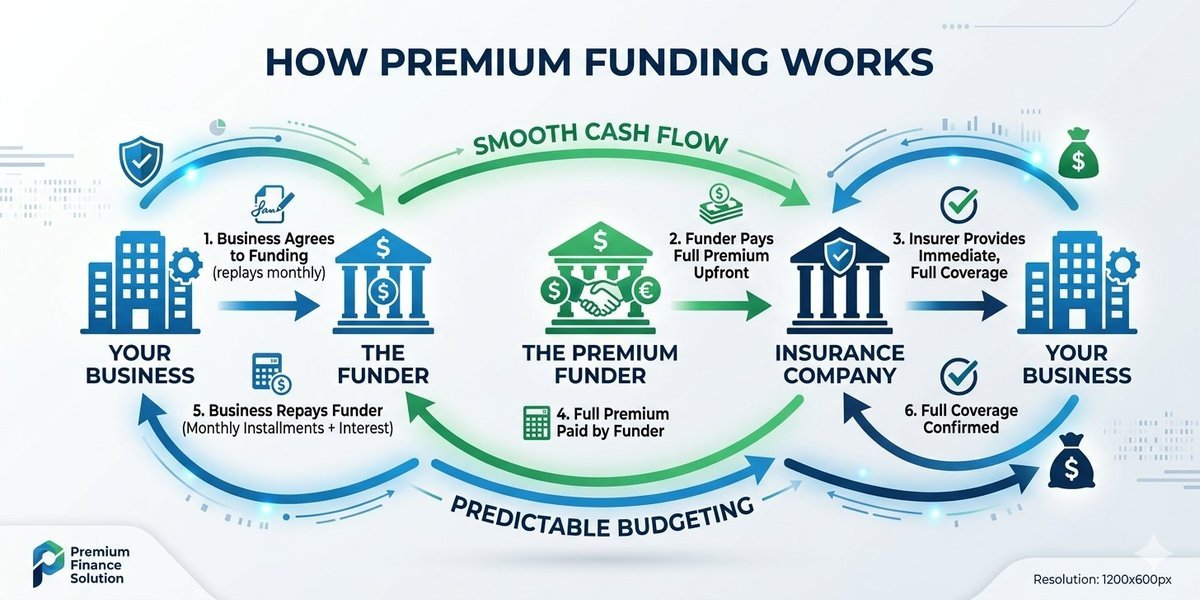

Before we look at the perks, let’s get the basics down. Premium funding is an arrangement where a third-party finance provider—the funder—pays your insurance bill directly to your insurance company. You then pay the funder back over a set time. Usually, this happens in monthly installments over 10 or 12 months.

Think of it like a short-term business loan. But the money never hits your bank account. It goes straight to the insurer. You get full coverage immediately, and you pay in smaller, bite-sized amounts. It’s a way to keep your protection without losing your shirt on day one.

1. It Keeps Your Cash Flow Strong

Cash flow is the lifeblood of any company. Everyone says it because it’s true. When you pay a massive insurance bill upfront—say $100,000—that is a huge chunk of cash leaving your business at once. It stresses out your payroll and makes vendor payments harder. So it just hurts.

Premium funding stops that pain. By spreading that cost, you keep your cash where it belongs: inside your operations. You aren’t just paying a bill; you are protecting your liquidity.

Did you know? A 2022 survey by PwC found that 63% of mid-size business executives ranked cash flow management as their top financial priority.

By using installments, you align your insurance costs with your monthly revenue. It’s much easier to manage.

2. Protecting Your Working Capital

Working capital is what you use to grow. It buys inventory, pays for marketing and funds new hires. The second you tie it up in a giant insurance payment, your options shrink. You become “cash poor” even if your business is successful.

For executives managing several policies, this problem gets worse. You might have:

- Commercial Property Insurance

- Public Liability

- Workers’ Compensation

- Directors and Officers (D&O) Insurance

The combined cost is often staggering. Premium funding protects your capital for things that actually make you money. Insurance is a necessity, but it doesn’t grow your business. Use your cash for things that do.

3. The Math: Return on Capital vs. Interest Rates

Look, here is the honest truth. Premium funding comes with an interest rate. You are paying a bit extra for the convenience. But for a smart executive, the math often works in your favor.

Let’s look at “Opportunity Cost.” If your business has a Return on Capital (ROC) of 15%, but the interest rate on the funding is only 7%, you are winning.

| Financial Factor | Traditional Upfront Payment | Premium Funding Strategy |

| Immediate Cash Outlay | 100% of Premium | ~8% to 10% (First Installment) |

| Impact on Liquidity | High | Low |

| Opportunity Cost | High (Cash is gone) | Low (Cash stays invested) |

| Interest Expense | $0 | Small Monthly Charge |

If you keep $100,000 in the business and earn more with it than the interest cost, the funding pays for itself. It’s a simple calculation that many students of finance should memorize.

4. Possible Tax Benefits

This is an area people often miss. In many countries, the interest you pay on premium funding is a tax-deductible business expense. The premium itself is just a cost of doing business, but the interest is a financing cost.

Tax rules change depending on where you are. Always talk to a pro before you bank on this. But generally, the tax deduction makes the net cost of the interest even lower. For a corporate executive, this makes the arrangement much more attractive during tax season.

5. Keeping Your Credit Lines Open

Most businesses have a line of credit or an overdraft for emergencies. You want to save those for the “big stuff”—unexpected opportunities or sudden crises. You shouldn’t waste your credit limit on a predictable, annual insurance bill.

Premium funding is a standalone facility. It does not touch your bank’s line of credit. It doesn’t show up on your credit card. This keeps your main credit lines free for when you really need them. It’s about keeping your financial “powder dry.”

6. Consolidating Multiple Policies

Managing insurance is a headache. If you have five different policies with five different renewal dates, your accounting team will hate you. One bill hits in March, another in June, and two more in October. It makes budgeting a nightmare.

One of the best parts of premium funding is consolidation. You can often roll all those policies into one single monthly payment.

- One date to remember.

- One payment to approve.

- One clear line item on your budget.

It turns a messy process into something clean and predictable. Finance teams love predictability. No more surprises when a renewal notice arrives in the mail.

7. Full Coverage From Day One

Some business owners try to delay insurance or take lower coverage to save money. That is a dangerous game. One uncovered fire or lawsuit could end the company.

With premium funding, the insurer gets paid in full immediately. You get your certificate of currency right away. You are 100% covered from the first minute. There is no waiting period and no “partial” coverage. You get the peace of mind of full protection without the immediate financial hit.

8. Speed and Simplicity

Have you ever tried to get a bank loan? It’s a slog. They want three years of tax returns, a business plan, and maybe your firstborn child as collateral. It takes weeks.

Premium funding is different. Usually, the “security” for the loan is the insurance policy itself. If you don’t pay, the funder cancels the policy and gets the refund from the insurer. Because they have that safety net, they don’t need to grill you. Approval often happens in 24 to 48 hours. The paperwork is minimal. For a busy executive, that speed is worth a lot.

Who Should Use This?

Honestly, almost any business can benefit. But it is especially huge for:

- Logistics and Shipping: Where fleet insurance costs are massive.

- Construction: High-risk industries with expensive liability cover.

- Seasonal Businesses: Companies that make most of their money in summer shouldn’t be paying huge bills in the winter.

- Growth-Phase Startups: When every dollar needs to go toward scaling.

The premium finance industry in the United States is huge. According to IBISWorld, it generates over $4 billion in annual revenue. It isn’t a niche tool anymore. It’s a mainstream way to handle corporate debt.

Potential Downsides to Consider

We have talked a lot about the good stuff. But let’s be real—nothing is perfect. You need to know the risks too.

- Interest Costs: You will pay more in total over the year. Check the rates.

- Cancellation Risk: If you miss payments, your insurance gets canceled. This is the biggest danger. You cannot afford to have a gap in your coverage.

- Fees: Look out for hidden setup fees. Read the fine print.

Always compare a few funders. Some have better rates or more flexible terms than others. Don’t just sign the first thing your broker puts in front of you.

Wrapping It Up

Managing the cost of insurance is a constant battle for business leaders. But premium funding offers a way to fight back. Instead of letting a giant bill drain your bank account, you turn it into a manageable, monthly expense. You protect your cash, keep your growth capital, and stay fully insured.

For students learning the ropes or executives looking for an edge, this is a key tool to understand. It isn’t just about paying a bill. It is a strategic move that supports both stability and long-term growth. If you haven’t looked into it yet, talk to your broker. It might be the smartest financial move you make this year.