Most people know they pay taxes. Few actually understand how much. And that gap can cost thousands. Your effective tax rate—the real percentage of your income going to the IRS—is rarely the same as your marginal bracket. In 2026, that gap just got wider for many high earners. The One Big Beautiful Bill Act (OBBBA), signed on July 4, 2025, made sweeping changes to the Alternative Minimum Tax (AMT). Some of those changes look friendly on the surface. But dig a little deeper and the picture gets complicated fast. This article breaks down the new math, shifts in phaseout rules, and the hidden traps that might push your actual tax bill higher than you ever expected.

What Is the AMT, and How Does It Work?

Think of the AMT as a shadow system. It runs parallel to the regular income tax rules. If your AMT bill ends up higher than your regular tax bill, you pay the AMT amount instead. Simple, right? Not really.

The AMT disallows certain deductions the regular system loves. Things like state and local taxes (SALT) and personal exemptions. That means more of your money is exposed to taxation under the AMT formula. Two rates apply: 26% and 28%. On the surface, that sounds low compared to the 37% top ordinary income rate. But the AMT applies to a much broader income base. That is exactly what makes it sting.

Before 2018, the AMT hit more than 5 million taxpayers every year. Then the Tax Cuts and Jobs Act (TCJA) of 2017 raised exemption amounts. The number of affected people collapsed to just 200,000 in 2018, according to KLR Tax Advisors. For a while, the AMT became a distant memory for most.

That changed with the OBBBA.

New Mechanics Under the OBBBA

The OBBBA made the higher AMT exemption amounts permanent. Look, on paper, that is great news. The 2026 exemptions are $90,100 for single filers and $140,200 for married couples filing jointly. This is a slight bump from the 2025 levels of $88,100 and $137,000 (IRS Revenue Procedure 2025-32). It helps shield middle-income earners from “bracket creep.”

But the law also brought two structural changes. These shift the burden heavily onto upper-income taxpayers.

The Phaseout Threshold Dropped Sharply

In 2025, the AMT exemption started disappearing at $626,350 for single filers. For married joint filers, it was $1,252,700. Starting January 1, 2026, those thresholds reset to $500,000 and $1,000,000.

That is a drop of over $126,000 for a single person. It happened overnight. Suddenly, a lot more of your income is “unprotected” by the exemption.

The Phaseout Rate Doubled

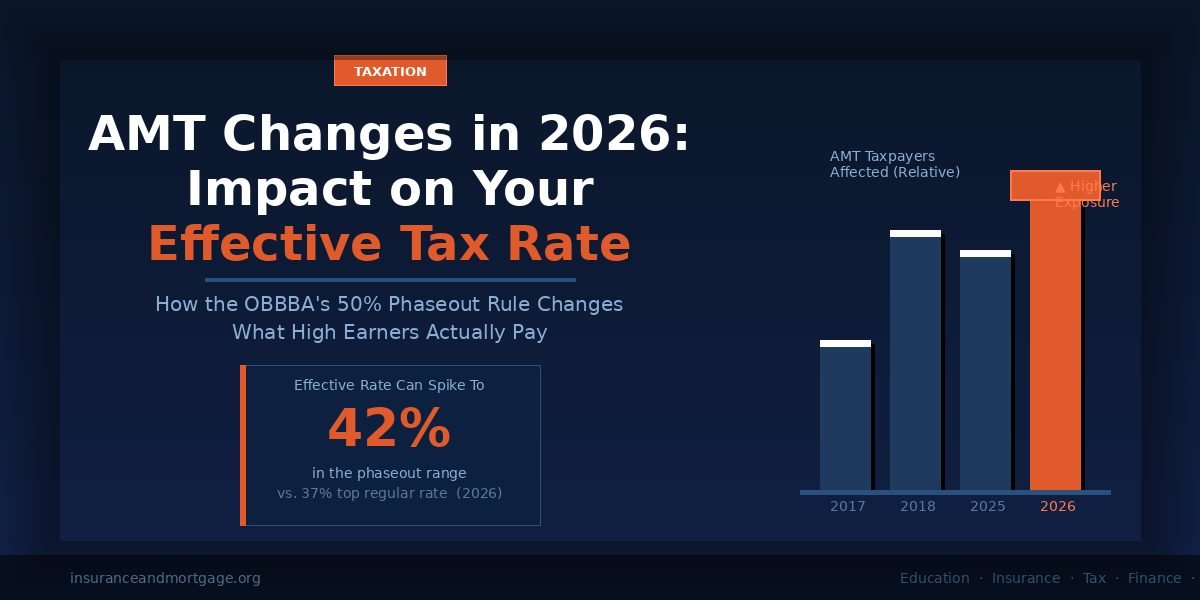

This is the part that really bites. Under the OBBBA, the rate at which the AMT exemption phases out doubles. It went from 25 cents per dollar to 50 cents per dollar (IRS Revenue Procedure 2025-32). Your exemption now vanishes twice as fast once you cross that threshold. Tax pros are calling this the “50% Bite Rule.”

How the 2026 AMT Affects Your Effective Tax Rate

Numbers matter here more than theory. Your effective tax rate is your total federal tax liability divided by your total income. It is not the rate on your last dollar earned. It is the average across everything you made. When the AMT kicks in, it pushes that average higher.

Here is a real example. According to Mercer Advisors, a taxpayer earning $600,000—with standard deductions like SALT and mortgage interest—had zero AMT liability in 2025 when exercising incentive stock options (ISOs). But waiting until 2026 to exercise those same options produces an extra $6,653 tax bill. No change in income. No change in deductions. Just the new phaseout rules doing their work.

For some taxpayers caught in the middle of the phaseout range, the effective marginal rate in that band can spike to 42%. That is higher than the 37% top regular rate. Let that sink in for a second. You are paying a higher percentage in a “lower” tax system.

The Hidden Impact of OBBBA “Fixes”

The OBBBA did more than just tweak the AMT. It changed how we itemize. But these “fixes” often act as bait for the AMT trap.

The SALT Deduction Paradox

The OBBBA raised the SALT deduction cap to $40,400 for 2026 (Tax Foundation). That sounds like a win for people in high-tax states. But SALT deductions are still worth zero under the AMT calculation. So, you claim a $40,400 deduction to lower your regular tax, which makes it more likely that your AMT bill will end up being the higher number. The two rules pull in opposite directions.

The New Charitable Floor

Starting in 2026, the OBBBA says charitable gifts must exceed 0.5% of your Adjusted Gross Income (AGI) before they are deductible. While charitable gifts are allowed under both systems, this new floor means you need to give more to see a tax benefit. It complicates the math for high-earning donors trying to lower their exposure.

The 35% Itemized Deduction Cap

There is another new rule for 2026. The tax benefit of itemized deductions is now capped at 35% for those in the top 37% bracket. If you are a high earner, your deductions just become less “efficient.” This adds even more upward pressure on your actual tax costs.

Who Is Most Exposed in 2026?

Not everyone needs to panic. But if your profile matches the list below, you should probably be running some projections.

- Single filers making over $500,000.

- Married couples making over $1,000,000.

- Anyone planning to exercise ISOs this year.

- High earners in high-tax states like New York or California.

- Taxpayers with large capital gains from selling a business or property.

Look, the SALT cap increase is a major trigger. If you take that expanded $40,400 deduction, you are basically inviting the AMT to take a look at your return. It is a classic “give with one hand, take with the other” scenario from the IRS.

What You Can Do About It

The good news is that AMT exposure is not a sure thing. You have some moves left on the board.

1. Time Your ISO Exercises

If you hold incentive stock options, do not just click “exercise.” Run a comparison of your 2025 and 2026 projections first. For some, exercising in 2025 was the clear winner. For others, waiting might work if 2027 looks like a lower-income year. Modeling this with a pro is not just a good idea—it is a requirement at this income level.

2. Accelerate Income into an AMT Year

This sounds crazy. Why would you want more income in a year you pay AMT? Because the max AMT rate is 28%. That is much lower than the 37% regular rate. If you know you are already hitting the AMT, pulling in short-term capital gains can actually save you money. The math supports it, even if it feels wrong.

3. Use the AMT Credit

If you pay AMT because of “timing items” like ISOs, you might get an AMT Credit. This credit can lower your regular tax in future years. It is a bit like a “tax prepay.” It does not help your cash flow today, but it provides a silver lining for tomorrow.

4. Bunch Your Giving

Since there is a new 0.5% floor for 2026, don’t spread your donations out. Bunch them into a single year to blow past that floor and get the full deduction. This works under both tax systems and helps offset the higher AMT exposure.

Wrapping It Up

The 2026 tax year is a turning point. We saw the phaseout threshold for single filers drop by over $126,000. We saw the phaseout rate double. And for high-income earners, the cumulative effect is a direct hit to the wallet.

There is a bigger lesson here for students and executives. Your tax bracket is not your effective tax rate. The gap between those two numbers is where real tax planning lives. The AMT has always shown us this, but in 2026, the gap turned into a canyon. If your income is anywhere near these new thresholds, do not wait for April. Run the numbers now while you still have time to change the outcome.